Sun Archives

Sun Coverage

Las Vegas will take much longer than the rest of the country to emerge from the recession, according to several local economists. And once it does, the good old days won’t be coming back.

Without a major effort to broaden and strengthen the foundation of the local economy, this is what they see as the new normal for Las Vegas: flat or at-best much slower population growth, higher-than-average unemployment, slow wage growth.

“We will lag the national economy instead of leading it,” UNLV economist Bill Robinson said.

In the past two decades, national recessions coincided with the opening of exciting new resorts — the Mirage in 1989 and the Palms after Sept. 11. These new visitor-magnets, combined with the steady migration of Americans toward the Sun Belt, helped blunt the effect of downturns.

This time, when the country finally awakes from its economic stupor, no such luck.

For one thing, California is the resort industry’s best customer base, and the economy there is as bad as it is here, with 11.6 percent unemployment, high rates of foreclosure, and homeowners who owe more on their homes than they are worth.

Nationally, Americans will have less discretionary income to spend on big-ticket items, such as trips to Las Vegas, because the debt binge is finished, said Jeremy Aguero, principal of the economics consulting firm Applied Analysis.

John Restrepo, vice chairman of the state’s official forecasting body the Economic Forum, said he believes there is a “fundamental shift” in American attitudes toward spending and debt, with at least marginally more conservative views taking hold.

Even once the business starts coming back, “We have excess capacity and excess labor supply,” said Keith Schwer, director of The Center for Business and Economic Research at UNLV.

The opening of CityCenter, which would otherwise offer a moment of hope, will exacerbate a problem — too many hotel rooms. An influx of visitors won’t likely fill up all the new hotels. By the end of 2011, there will be more than 16,000 hotel rooms added to the 140,000 in inventory at the beginning of this year, plus innumerable condo-hotel towers and time share units that add to the total.

All the new capacity will further force down room rates, well below what investors assumed in their projections as they designed the projects.

At mid-level properties, rooms will go for a song.

With low room rates cutting into profit margins, as well as a tight credit market, there will likely be no new projects for years, and mid-level properties will struggle to find money to renovate.

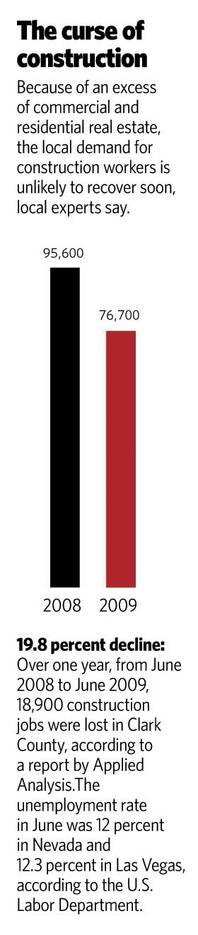

Operators will have one advantage: The Clark County unemployment rate is 12.3 percent, and that doesn’t count all the people who have stopped trying or are working part-time even though they would rather be full-time, thus pushing the effective rate near 20 percent, or “Great Depression numbers,” as Robinson put it. This will give management significant leverage over workers, which will depress wages.

With high unemployment and no new Strip projects, fewer people in search of opportunity will come here.

Less growth will hurt demand for new housing.

Given the glut of commercial property — empty strip malls and office complexes — there will be little need to build any of that anymore.

The upshot: The tourism and hospitality industries will slowly recover, but construction won’t.

This comes after a decade in which construction and development were seen as a strong second pillar of the Southern Nevada economy.

Instead, Las Vegas will again be a one-trick pony, albeit with a more opulent saddle than the previous version.

It turns out the assumption that construction and development could be a second pillar of our economy was foolish, economists say.

“It sounds pretty unsustainable when you think about it,” said Elliott Parker, an economist at the University of Nevada, Reno. “Construction workers building houses for construction workers who were here to build houses for other construction workers.”

It was all predicated on home prices rising forever.

To paraphrase the late economist Herbert Stein, things that can’t go on forever, don’t.

•••

So what now?

There is some hope that the old growth model might deliver some relief, if not right away, then in the medium term.

Aguero has said he sees signs of optimism in the residential market, as robust home sales are finally outstripping new foreclosures, and prices seem to be stabilizing.

Also, the climate never hurts.

Lee McPheters, economist and director of the JPMorgan Chase Economic Outlook Center at the W.P. Carey School of Business at Arizona State University, said he expects that once the national economy begins to recover and people can sell their homes back East for a decent price, they will seek sunshine — and now, affordable homes — out West.

But the consensus among economists is that the state must pursue a new economic strategy, one that will produce a more sustainable prosperity.

Experts say Las Vegas has two options.

One is to wring more out of travel, tourism and conventions.

To some extent, the city is working that angle, and with some success.

“Las Vegas has repositioned itself as a substitute good,” Aguero said. “Come and spend your tourism dollars here because they will go farther than in Paris or New York.”

The recession is clearly lighting a fire under operators to be more creative, while also offering better rates.

More needs to be done, Robinson said. He said too many properties are essentially the same. Spacious, opulent lobby, pool and club debauch, restaurants and gaming tables.

Harrah’s proposed pedestrian mall with bars and restaurants is a nod in a new direction. A big-time amusement park would be another.

Policymakers can also hope to make the city more of a business hub for the travel and tourism industry, with more airline and hotel corporate headquarters, or startup software companies that would service the hospitality industry.

These developments would create high-paying jobs for educated, highly skilled workers.

Las Vegas needs more of these educated workers because, as the current recession has shown, low-skill jobs are more likely to get eliminated in a downturn. Robinson noted that the national unemployment rate for college-educated workers is 4.7 percent, roughly half the overall rate.

The other option for Las Vegas is to move into nontourism and travel — the longtime holy grail of economic diversification.

In some respects, elected officials and other policymakers have been trying to do this for decades, with mixed results.

The Nevada Development Authority has a long list of companies that have arrived in the past decade, often for the state’s favorable regulatory and tax climate — Nevada is one of a few states without a corporate or personal income tax.

Among the companies are warehousing and call centers, medical firms and energy companies. Zappos.com, the online shoe company just bought by Amazon.com, is a cause for real optimism, they say, because it is a next-generation company that relies on a resource in abundance in Las Vegas — customer service.

Lt. Gov. Brian Krolicki, whose primary duty is to draw new businesses here, said Nevada’s friendly tax and regulatory environment and California’s problems continue to create fertile ground for recruiting new companies.

He has 260 leads, of which 40 percent are renewable energy companies interested in research and development, manufacture of equipment and energy generation, he said.

(Renewable energy is a constant refrain of elected officials, although some experts say it won’t lead to much job creation because the facilities require very little labor once they’re built.)

But while the development authority (phone number: (888) 4-NO-TAXES or (888) 466-8293) and Krolicki tout the state’s low-tax environment, economists here say diversification efforts can’t ignore the role of taxpayer-funded education in economic development.

“There are no simple answers when you’re dead-last in education, when education and technology are the ways you grow,” said Schwer, referring to Southern Nevada’s schools and the state’s struggling universities.

There are two key moments in the rise of American economic dominance, Schwer noted. Mandatory schooling led to a rapid rise in literacy; innovation and engineering feats followed.

Then, after World War II, millions of young men went to college on the GI Bill, and a new period of innovation and domination followed.

Schwer noted that Nevada has succeeded at seeking out new opportunities before, with railroads and the hunt for water, the dam and the Henderson war plants. Then there was the great entrepreneurial wave of the past 20 years, when titans of tourism battled it out to bring an ever more fanciful product to a bigger and bigger paying crowd.

Schwer, Robinson and Elliott offered similar prescriptions: investments in education, health care, culture and infrastructure, creating an environment in which innovators — be it in tourism or something else — can thrive.

The alternative, Restrepo said, is grim. “Without fundamental changes, investments in education and economic diversification, it’s not a great outlook.”

Join the Discussion:

Check this out for a full explanation of our conversion to the LiveFyre commenting system and instructions on how to sign up for an account.

Full comments policy